In order to tackle rising inflation, the Bank of England (BoE) has raised the base interest rate 13 consecutive times since December 2021. As of June 2023, it now stands at 5%.

Rising interest rates is one of multiple factors that has called UK mortgage affordability into question over the past year. Others include:

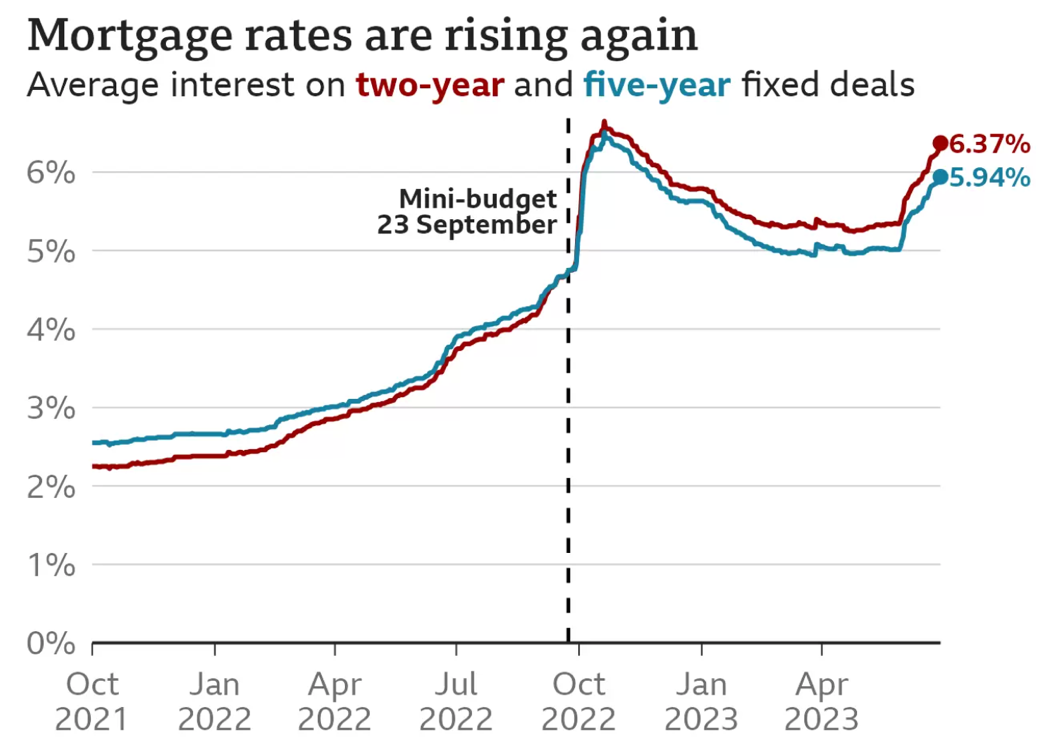

- Former chancellor Kwasi Kwarteng’s controversial mini-Budget in September 2022. This event pushed two-year fixed mortgage rates to their highest levels since 2008, the Guardian reports.

- Rising house prices. The Office for National Statistics (ONS) found that UK house prices grew by 1.9% in the year to May 2023, down from 3.2% in April.

- The cost of living crisis. Inflation stood at 7.9% as of June 2023, after peaking at 11.1% in October 2022, the ONS states. This reflects what has been called the “cost of living crisis” as everyday costs have risen sharply.

Keep reading to find out how mortgage repayments have changed as a result of the above factors, and what the government is doing to help customers stay in their homes.

Mortgage repayments have increased steeply in the past 12 months

Although the subject of mortgage affordability is now coming to a head in the news, circumstances began to change in 2022.

With interest and inflation on the rise and political upheaval causing markets to fluctuate, the ONS reports that monthly repayments on an average semi-detached house rose by 61% last year.

The below chart shows how Kwasi Kwarteng’s September mini-Budget acted as a catalyst for the already-rising cost of two- and five-year fixed mortgage deals.

Source: BBC News

In the mini-Budget, the former chancellor announced a series of drastic measures, including the abolition of additional-rate Income Tax, many of which have now been reversed – but not before mortgage markets had the chance to react.

Fast forward to June 2023, and according to a report in the Guardian, more than a million mortgage holders could lose up to 20% of their disposable income to surging mortgage costs.

What’s more, in May, Which? reported that home repossessions were up by 50%, reflecting a worrying level of precarity for homeowners up and down the UK.

A new government charter is set to help homeowners who are struggling to pay their mortgage bills

After public pressure to act on the side of struggling homeowners, the government met with key mortgage lenders to put together a package of support.

The new mortgage charter provides support for residential mortgage customers, and includes several important commitments. The lenders involved cover 75% of the market, the government says.

Here are five key takeaways from this new measure.

1. Worried customers can call their lender for support

Under the new mortgage charter, borrowers who are worried about affording their bills can call their lender or bank for information and support.

Crucially, these interactions will have no impact on your credit score.

2. You can secure a new fixed-rate deal up to six months before your existing agreement ends

In a measure designed to help those needing to remortgage soon, fixed-rate mortgage customers can now find and lock in a new fixed-rate deal in the six months leading up to their current agreement ending.

This means that if you anticipate that rates may rise again before you’re due to remortgage, you can agree a deal now and spend the coming months preparing for your new rate.

What’s more, if a more affordable deal comes up within that six-month period, customers are free to pursue new agreements right up until their remortgage date.

3. Some customers can switch to an interest-only mortgage to reduce their monthly payments

A new agreement between lenders, the Financial Conduct Authority (FCA) and the government allows customers to switch to an interest-only mortgage for six months. They can also extend their mortgage term to reduce their monthly payments and switch back to their original term within the first six months, if they choose to.

Both these routes can be taken without a new affordability check, and neither will affect your credit score. This means you may not have to worry about how this choice could affect your future borrowing options.

4. Some mortgage holders may be able to remortgage without an affordability check

The government says it will provide “support for customers who are up to date with payments to switch to a new mortgage deal at the end of their fixed-rate deal without another affordability check”.

This measure could ensure you are able to get the mortgage that’s right for you when your term ends, without feeling concerned that your finances won’t make the cut on paper.

5. Customers won’t be forced to have their homes repossessed 12 months after their first missed payment

Under this new charter, mortgage holders won’t be forced to have their homes repossessed within 12 months from their first missed payment. This could provide immense peace of mind for those who are struggling to keep up with repayments in the short term.

If you are buying a home or remortgaging this year, speaking to a professional could make all the difference

Although the government’s new measures could provide welcome relief to stressed homeowners, remortgaging or buying a new home in the current climate could still be a little overwhelming.

Fortunately, working with an experienced mortgage broker can help put your mind at ease. I can:

- Access a wide range of lenders who may be able to provide a deal that suits your situation

- Talk through your options whether you’re buying your first home, expanding your property portfolio, or remortgaging on your current residence

- Answer any questions you may have about the mortgage market and house prices.

Rather than facing the mortgage market by yourself, having a professional ally on your side can make all the difference.

Get in touch

You can’t put a price on peace of mind – so if you’re looking for a new mortgage, get in touch with us today.

Email enquiry@edinburghmortgageadvice.co.uk or call 0131 339 2281 to speak to us.

Please note

This article is for information only. Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

Your home may be repossessed if you do not keep up repayments on a mortgage or other loans secured on it.

Buy-to-let (pure) and commercial mortgages are not regulated by the FCA.

Think carefully before securing other debts against your home.