In the world of financial transactions, especially when securing a mortgage, one’s credit file stands as a testament to their financial behaviour and trustworthiness. Yet, it’s a common misconception that only ‘perfect’ credit will pave the way for smooth mortgage approvals. Let’s shed some light on the matter.

Your credit file is a comprehensive record of your borrowing history. This details all your financial commitments, past repayments, and any outstanding debts. Mortgage lenders rely on this information to gauge your reliability as a borrower. However, what many individuals don’t realise is that very few people possess what can be considered a ‘perfect’ credit file. Life is full of unexpected twists, and sometimes events out of our control can leave a dent in our credit history.

Fortunately, mortgage lenders are well aware of this reality. They understand that not every missed payment or financial hiccup represents a risk. As such, there exists a spectrum of lenders, many of whom are more than willing to consider applicants whose credit histories are less than immaculate. They evaluate the broader pictur, so taking in your current financial stability and any blemishes on your credit file.

In light of this, it’s paramount to understand and regularly review your credit. Being well-informed empowers you to make the best decisions for your financial future and ensure you’re not left in the dark about where you stand.

Recommendation:

Before you embark on your mortgage journey, arm yourself with knowledge. Obtain a copy of your credit file and understand your financial standing.

For anyone without access to their file here is an offer of the 30 day free trial and £14.99 per month after that. You have the ability to cancel the trail or subscription at anytime. – Click here to access your credit report

If you download your file then we will very happy to give you mortgage advice based on this information. Please call 01313392281 or complete the below form.

With the warmer weather here, now is the perfect time to get outside and spend some time improving your outdoor space. Planting new trees and shrubs is an excellent way to spruce up your garden, and doing so can even greatly benefit the environment.

It seems as though many are planning on doing this, too – Aviva reports that 33% of UK residential gardens expect to see new trees, hedges, or shrubs introduced this year.

Before you head out and put your green fingers to good use, it’s important to be aware of potential subsidence risks, especially if you plan on planting new wooded foliage.

Continue reading to discover why planting trees and shrubs near your home may result in subsidence, and how you could potentially avoid it.

Subsidence can cause the foundations of your home to sink

Subsidence occurs when the ground beneath your property sinks, often causing damage to its foundations. This commonly happens during warmer spells, as the heat can dry out the soil, leading to shrinkage.

Certain soil types are often more susceptible to subsidence – clay soils, in particular, tend to crack and shift more during prolonged dry spells. Additionally, some tree and shrub species can sometimes accelerate subsidence, as many absorb more water and dry out the soil more quickly.

It may be prudent to take any measures necessary to avoid subsidence. Home Selling Expert states that the average cost to repair sinkage is around £6,000 to £14,000, though more severe cases could cost as much as £50,000.

To identify subsidence, you should keep an eye out for any cracks in the walls of your home. Cracks caused by subsidence are more distinctive than others, as they are typically wider at the top than at the bottom, and can more often be found around doors and windows.

Some helpful tree and shrub tips that could help you reduce the chance of subsidence

Before you plough ahead and introduce some new greenery to your property’s surroundings, it may first be wise to consider the type of tree or shrub you plant.

As you read earlier, certain species with a higher water demand can accelerate subsidence, including:

Poplar

Willow

Elms

Oak

So, it may be worth planting trees and shrubs with shorter root structures and lower water demand, such as:

Birch

Elder

Hazel

Magnolia

When you’ve decided which tree or shrub would best suit your garden, the next thing to consider is where to plant them. You should ideally be as strategic as possible when choosing their location – planting them close to your home or garage can give roots more opportunity to damage your property.

And, if you already have trees or shrubs, it may be wise to pollard them. This is essentially a method of pruning that thins out branches and reduces trees and shrubs’ water demand, allowing the soil to retain more water.

Ultimately, paying attention to how and what you plant near your property can help avoid expensive issues down the line.

Get in touch

If you would like some expert advice on any mortgage matters or how to maintain a healthy home, please get in touch with us.

The UK’s buy-to-let landscape has changed significantly since the pandemic.

According to data published by the Office for National Statistics (ONS), private rental prices increased by 5.1% in the year to June 2023. But in some areas, the Guardian reports, rents have been hiked by as much as 20% this year.

Many of these rent price increases are being implemented as a direct result of rising mortgage costs. The Bank of England (BoE) brought the base interest rate from 0.1% to 5% between December 2021 and June 2023. Unsurprisingly, as a result, as of 19 July 2023 the best rate available on a two-year fixed-rate mortgage deal was 6.39%, with five-year deals available at a minimum of 5.69%, Moneyfacts states.

All this to say: if you are a landlord with multiple properties, you may be finding it difficult to shoulder increasing monthly repayments.

Aside from this central challenge, though, 2023 has also brought some lesser-known rule changes that buy-to-let landlords should be aware of.

So, if you’ve been focusing on price rises, you may have missed these two key rule changes to the UK rental market.

1. Energy Price Certificate rules have tightened

An Energy Price Certificate (EPC) shows how energy-efficient your property is. It looks at how well the home retains heat, and its CO2 emissions.

Starting in April 2023, all rental properties (including those under ongoing tenancies) must meet the government’s Minimum Efficiency Standards, which means they should have an EPC rating of “E” or above.

And, from April 2025, landlords must update their homes if necessary to meet an EPC rating of “C”. This will apply to new tenancies, and come into force for ongoing tenancies in April 2028.

So, if your rental homes currently have an EPC rating of “E”, you’re out of the woods for now.

However, by 2025, you may need to make the necessary renovations to achieve a “C” score if you wish to keep your properties tenanted in future.

2. Pet regulations are shifting in favour of tenants

“Well-behaved pets” have been allowed into Scottish rental properties since the new Model Private Residential Tenancy Agreement was produced by the government in 2020. Under this agreement, while landlords can still refuse pets in extenuating circumstances, tenants in Scotland may no longer face a blanket ban on having pets in their rented home.

In England, meanwhile, similar reforms are only just coming into force. The government’s Renters (Reform) Bill, proposed in May 2023 and set to be passed in 2024, “will ensure landlords do not unreasonably withhold consent when a tenant requests to have a pet in their home, with the tenant able to challenge unfair decisions”.

The bill also states that landlords will be allowed to request additional insurance if a tenant wishes to have animals on the property, to ensure that any pet damage caused will be covered by the tenant.

This bill, if passed, may see an end to total pet bans on rental properties in England.

So, if you have properties in Scotland or England, it’s important to note that you may no longer be able to refuse your tenants’ pet requests unless there are behavioural or welfare concerns. If you do refuse, your tenant can make a legal appeal.

Get in touch

If you’re a landlord wishing to expand your property portfolio, or you’re worried about the current mortgage climate, contact us today. Email enquiry@edinburghmortgageadvice.co.uk or call 0131 339 2281 to speak to us.

Please note

This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

All contents are based on our understanding of HMRC legislation, which is subject to change.

Your home may be repossessed if you do not keep up repayments on a mortgage or other loans secured on it. Buy-to-let (pure) and commercial mortgages are not regulated by the FCA. Think carefully before securing other debts against your home.

In order to tackle rising inflation, the Bank of England (BoE) has raised the base interest rate 13 consecutive times since December 2021. As of June 2023, it now stands at 5%.

Rising interest rates is one of multiple factors that has called UK mortgage affordability into question over the past year. Others include:

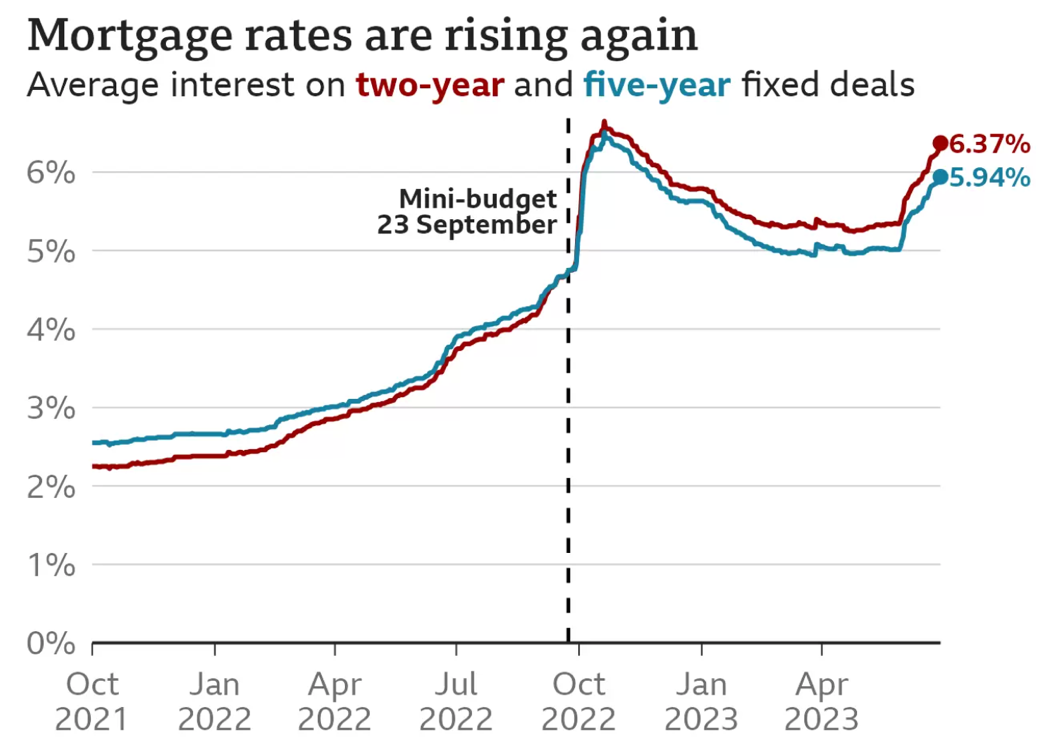

Former chancellor Kwasi Kwarteng’s controversial mini-Budget in September 2022. This event pushed two-year fixed mortgage rates to their highest levels since 2008, the Guardian reports.

Rising house prices. The Office for National Statistics (ONS) found that UK house prices grew by 1.9% in the year to May 2023, down from 3.2% in April.

The cost of living crisis. Inflation stood at 7.9% as of June 2023, after peaking at 11.1% in October 2022, the ONS states. This reflects what has been called the “cost of living crisis” as everyday costs have risen sharply.

Keep reading to find out how mortgage repayments have changed as a result of the above factors, and what the government is doing to help customers stay in their homes.

Mortgage repayments have increased steeply in the past 12 months

Although the subject of mortgage affordability is now coming to a head in the news, circumstances began to change in 2022.

With interest and inflation on the rise and political upheaval causing markets to fluctuate, the ONS reports that monthly repayments on an average semi-detached house rose by 61% last year.

The below chart shows how Kwasi Kwarteng’s September mini-Budget acted as a catalyst for the already-rising cost of two- and five-year fixed mortgage deals.

In the mini-Budget, the former chancellor announced a series of drastic measures, including the abolition of additional-rate Income Tax, many of which have now been reversed – but not before mortgage markets had the chance to react.

Fast forward to June 2023, and according to a report in the Guardian, more than a million mortgage holders could lose up to 20% of their disposable income to surging mortgage costs.

What’s more, in May, Which? reported that home repossessions were up by 50%, reflecting a worrying level of precarity for homeowners up and down the UK.

A new government charter is set to help homeowners who are struggling to pay their mortgage bills

After public pressure to act on the side of struggling homeowners, the government met with key mortgage lenders to put together a package of support.

The new mortgage charter provides support for residential mortgage customers, and includes several important commitments. The lenders involved cover 75% of the market, the government says.

Here are five key takeaways from this new measure.

1. Worried customers can call their lender for support

Under the new mortgage charter, borrowers who are worried about affording their bills can call their lender or bank for information and support.

Crucially, these interactions will have no impact on your credit score.

2. You can secure a new fixed-rate deal up to six months before your existing agreement ends

In a measure designed to help those needing to remortgage soon, fixed-rate mortgage customers can now find and lock in a new fixed-rate deal in the six months leading up to their current agreement ending.

This means that if you anticipate that rates may rise again before you’re due to remortgage, you can agree a deal now and spend the coming months preparing for your new rate.

What’s more, if a more affordable deal comes up within that six-month period, customers are free to pursue new agreements right up until their remortgage date.

3. Some customers can switch to an interest-only mortgage to reduce their monthly payments

A new agreement between lenders, the Financial Conduct Authority (FCA) and the government allows customers to switch to an interest-only mortgage for six months. They can also extend their mortgage term to reduce their monthly payments and switch back to their original term within the first six months, if they choose to.

Both these routes can be taken without a new affordability check, and neither will affect your credit score. This means you may not have to worry about how this choice could affect your future borrowing options.

4. Some mortgage holders may be able to remortgage without an affordability check

The government says it will provide “support for customers who are up to date with payments to switch to a new mortgage deal at the end of their fixed-rate deal without another affordability check”.

This measure could ensure you are able to get the mortgage that’s right for you when your term ends, without feeling concerned that your finances won’t make the cut on paper.

5. Customers won’t be forced to have their homes repossessed 12 months after their first missed payment

Under this new charter, mortgage holders won’t be forced to have their homes repossessed within 12 months from their first missed payment. This could provide immense peace of mind for those who are struggling to keep up with repayments in the short term.

If you are buying a home or remortgaging this year, speaking to a professional could make all the difference

Although the government’s new measures could provide welcome relief to stressed homeowners, remortgaging or buying a new home in the current climate could still be a little overwhelming.

Fortunately, working with an experienced mortgage broker can help put your mind at ease. I can:

Access a wide range of lenders who may be able to provide a deal that suits your situation

Talk through your options whether you’re buying your first home, expanding your property portfolio, or remortgaging on your current residence

Answer any questions you may have about the mortgage market and house prices.

Rather than facing the mortgage market by yourself, having a professional ally on your side can make all the difference.

Get in touch

You can’t put a price on peace of mind – so if you’re looking for a new mortgage, get in touch with us today.

This article is for information only. Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

Your home may be repossessed if you do not keep up repayments on a mortgage or other loans secured on it.

Buy-to-let (pure) and commercial mortgages are not regulated by the FCA.

Think carefully before securing other debts against your home.

Skipton Building Society have launched a new mortgage, ‘The Track Record,’ where the buyers do not need a deposit.

The product’s aim is to answer the complaint ‘we cannot save a significant deposit is because they are paying such high rental payments.’ that is made by people renting property. A catch 22 for people in this space.

The Skipton’s answer is that as long as your new mortgage payment is below you previous average rental payment and you can pass the affordability test, then you are able to apply for the 100% scheme.

Getting First Time Buyers moving

At launch this is a 5 year fixed rate at 5.59% with no set up fee, our view on why a 5 year fix is that these are cheaper currently than 2 year fixes and protect buyers against any volatility in the bhousing market over the next couple of years.

There are other hurdles that need to get covered off

Each applicant is a first time buyer

Each applicant is aged 21 or over

If they have a deposit, it must be less than 5% of the purchase price

Each applicant has no missed payments on debts / credit commitments (e.g. mobile phone bill) in the last 6 months

They are looking to borrow up to £600,000

They meet the household-to-household criteria (see below)

They’re not looking to buy a new build flat

They have proof of having paid rent for at least 12 months in a row, within the last 18 months

They have 12 months experience paying all household bills within the last 18 months.

You can have up to 4 applicants on the mortgage, but they will need to evidence the rental payments made over the last 12 months.

Joint applicants who have rented seperately will be eligible, but again need to evidence the rent and household expenditure payments. In this case the retnal payments are added together for the loan calculation purpose.

If you are interested in this or any other product please give us a call on 01313392281 or email mark@edinburgh.mortgage

If you are a homeowner, your monthly mortgage payments may have increased in the last few months. Or, perhaps your fixed-rate deal is coming to an end and you’re concerned about what your repayments will be at that time?

Similarly, if you are a planning on buying a house, you need to know how best to minimise the impact that rising interest rates and mortgage repayments will have when taking your first or next steps on the property ladder.

Due to the uncertainty over the UK economy and rising inflation, sat at 10.1% as of March 2023, it is now more important than ever to shop around and find the most suitable way of reducing your monthly mortgage repayments. One of the ways that could help you achieve this is an offset mortgage.

But what exactly is an offset mortgage, and would it be the best option for you? Read on to find out.

An offset mortgage is a type of mortgage that’s linked to your savings account

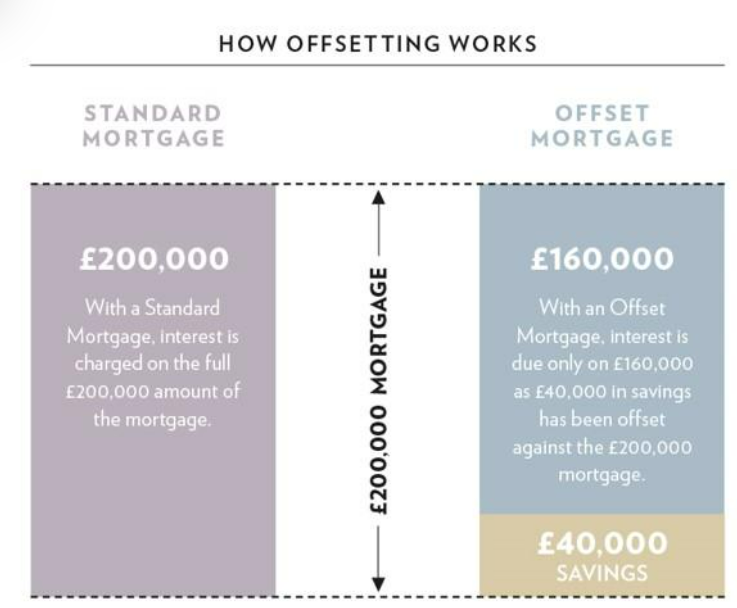

When you choose an offset mortgage, you can link your bank and savings accounts to your mortgage. Any money in your linked savings accounts will lower the total interest you will be charged – hence “offsetting” your mortgage balance.

Essentially, the offset mortgage treats the amount of savings you have as if it was “credit” on your mortgage – as the graphic below shows.

If you have cash saved for a rainy day or a purchase that won’t be required soon, an offset mortgage could be ideal. The surplus funds could be used to reduce the interest you pay on your mortgage.

Using the example from the graphic above, if you have a typical £200,000, 30-year capital and interest mortgage at a rate of 2.19%, your monthly mortgage repayments would be £758.39 each month.

However, if you have an offset mortgage and £40,000 in your linked savings account, your monthly mortgage repayments would be £73 cheaper, at £685.39 each month.

Alternatively, you could choose to keep your monthly mortgage repayments at £758.39. Using the example above, you would finish repaying your mortgage four years earlier using this strategy.

What you need to consider

If you’re thinking about choosing an offset mortgage, one possible downside is that you may pay a higher interest rate. Offset mortgages often have higher initial rates than their alternatives, meaning your standard monthly repayments might not be as low as a more traditional option.

Alongside that, it’s unlikely that you will earn interest on the savings in your linked account. The money will be used to reduce the interest charged on your mortgage, so unlike with a Cash ISA or a traditional savings account, you won’t see these savings grow.

Get in touch

As with any house buying or remortgaging decision, it’s always a good idea to speak with us before you act. We can help you investigate the best options available to you and choose the most suitable mortgage for your circumstances.

In his spring Budget on 15 March, the chancellor, Jeremy Hunt, announced that he would extend the Energy Price Guarantee (EPG) until the end of June 2023.

So, what exactly does that mean for your bills and what will happen at the beginning of July? Read on to find out.

The EPG extension will keep the average bill at £2,500 a year

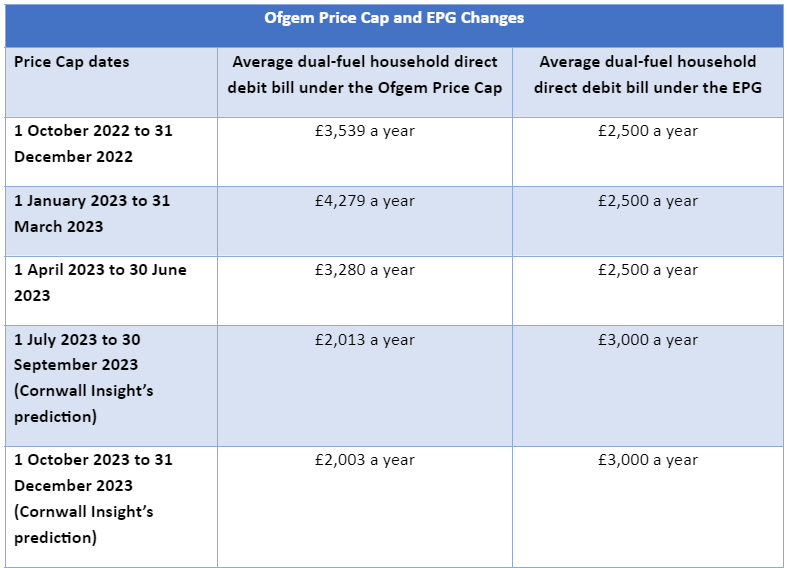

The Ofgem price cap, introduced on 1 January 2019, set the average cost of annual standard variable energy tariffs in the UK to £1,137. Over the years since, this has steadily increased, with the average cost now £3,280 as of April 2023.

In a bid to help households with these sharp rises in the cost of gas and electricity, the former prime minister, Liz Truss, launched the EPG on 1 October 2022. This scheme limited what an average UK household would pay annually for electricity and gas to around £2,500 in Great Britain and around £2,109 in Northern Ireland.

According to the government’s official figures, “the EPG will have saved a typical household in Great Britain around £1,100 since the scheme began in October 2022, compared to undiscounted energy prices under the price cap.”

Alongside this, an Energy Bill Support Scheme was introduced to provide households with £400 of account credit or a reduction in direct debit payments. If your supplier provided this funding between October 2022 and March 2023, you will have noticed that your monthly energy bills have increased by either £66 or £67 since April 2023.

The chancellor’s spring Budget announcement will keep the EPG at £2,500 until 1 July, with the government estimating that the average UK household will save £160 compared to the energy prices under the Ofgem price cap.

But what will happen to your energy bills come 1 July?

From 1 July, you will pay the lower of either the EPG (which will be set to £3,000 a year until the end of March 2024) or the Ofgem price cap, currently set to £3,280 a year.

While energy prices are 50% lower than when initially forecast in October 2022, the average UK household will likely still see an annual increase of either £500 or £780 to their gas and electricity bills from 1 July 2023.

Thanks to lower wholesale gas prices, Cornwall Insight is predicting that the Ofgem price cap will be reduced to an estimated £2,100 a year for an average UK household later in 2023. If these forecasts prove correct, you could save up to £400 on average on your energy bills each year compared to what you are paying under the EPG.

Please note

This article is for general information only and does not constitute advice. The information is aimed at retail clients only.

If your mortgage payments have gone up in the last year, you’re not alone.

Since December 2021, the Bank of England (BoE) has raised the base rate 11 times, with the rate standing at 4.25% as of April 2023, compared to 0.1% back in late 2021.

Since Kwasi Kwarteng’s mini-budget in September 2022, mortgage rates have been steadily increasing and, according to the Office for National Statistics (ONS), mortgage repayments for the average semi-detached house in the UK rose by 61% in 2022.

In addition to that, the number of mortgage approvals granted in January 2023 sank to its lowest level since the financial crash of 2008, following a downward trend lasting five months.

So, if your mortgage repayments have risen in recent months, or you’re concerned about what will happen when your current deal ends, here are three options you can consider.

1. Review your tracker- or variable-rate mortgage today

With the BoE regularly increasing the base rate since December 2021, it’s highly likely that your mortgage repayments will have gone up if you’re on a tracker or variable rate. So, it can be worth reviewing your options to see what else might be available.

This can help you find a deal that could save you money, or possible protect you against further interest rate rises in the future.

Given that tracker- and variable-rate mortgage payments are typically tied to base rate rises and falls (although a lender can independently raise their standard variable rate (SVR)), choosing the right mortgage for you will depend on your own personal circumstances.

If you expect interest rates to fall in the upcoming months, sticking with a tracker- or a variable-rate mortgage could be the best option for you, as it might mean your repayments fall if interest rates fall. However, if you want the security of knowing exactly what you will pay for a set period, a fixed-rate deal might be more appropriate.

As an independent expert, we can help you review the options available to you. We can scour the market and help you to find the most appropriate mortgage for your needs.

2. Shop around now if your fixed-rate deal is coming to an end soon

If you currently have a fixed-rate mortgage and it’s due to end in the coming months, now is the time to start considering your options and shopping around. If you don’t act, you will likely end up on your lender’s SVR, which will most likely mean your repayments will be higher than they are now.

It’s now more important than ever to review your current mortgage deal and explore all the options open to you. You can either take a new deal with your existing lender, potentially saving you time and hassle, or switch to a new provider.

Sticking with your current provider can sometimes be of benefit. Often, it’s quicker to agree a new deal with your existing lender and it may be easier to get a deal approved with a lender that already knows and trusts you, compared to one that you’ve never dealt with before.

However, the deal your existing lender may offer you might not be competitive, and there could be other options that could save you hundreds or even thousands of pounds over the next few years.

Bear in mind that many mortgage offers are valid for six months, so if your deal ends in that window, now is the time to start investigating and researching all your options.

Due to the uncertain nature of the UK economy in 2023, Forbes has reported that many lenders are attempting to attract new customers with reduced fixed-rate deals. So, make sure you talk to us before you act, as we can advise you on all the offers available to you and help you find the right one for you – whether that’s with your current lender or a new one.

3. Run through the choices open to you with an experienced mortgage broker

When making any kind of important financial decision, it’s always wise to seek advice and guidance from an experienced professional that knows the topic inside-out. We can work with you to explore your options and find the most suitable mortgage option for you.

With interest rates rising over the last 12 months and mortgage repayments typically higher on average, it’s important to be armed with all the information you need to make the right decision if your mortgage deal comes to an end soon.

So, if your current deal is ending in 2023, speak to one of our experienced mortgage experts today. Email enquiry@edinburghmortgageadvice.co.uk or call 0131 339 2281.

Please note

Your home may be repossessed if you do not keep up repayments on a mortgage or other loans secured on it.

With the average price of a home increasing consistently throughout the last few decades, first-time buyers are facing serious affordability challenges.

If you have been keeping an eye on mortgage rates since the end of 2022, you will know that there were some headline-worthy market shifts in recent months.

YOUR HOME MAY BE REPOSSESSED IF YOU DO NOT KEEP UP REPAYMENTS ON YOUR MORTGAGE OR OTHER LOANS SECURED ON IT

Any fee payable for our services will depend upon your circumstances. In these situations we will inform you during our initial discussions and detail it in the Our Service to You document. In these cases our usual fee is £395 (for Buy to Let mortgages it is £495).

Edinburgh Mortgage and Thistle Finance are trading styles of Mark Dyason who is authorised and regulated by the Financial Conduct Authority, and is entered on the FCA register (https://www.fca.org.uk/firms/financial-services-register) under reference 607668.